Over the last six months, I’ve been asked a lot about the national debt, and how sustainable that national debt may be over the next decade. Debt sustainability of any country is really about how world financial markets are willing (or not) to purchase any more of a country’s debt. A lack of demand means higher interest rates paid on new debt and sometimes a lack of salability. When government spending exceeds revenues, a fiscal deficit occurs and new national debt is issued to pay that difference, much like any business that faces a cashflow shortfall. Interest rates on American national debt are as low as you can find around the world. Generally speaking, this is due to the perceived low risk of default concerning other asset choices by investors in world financial markets. The next 10 years likely tell a tale of how stable our national debt market is.

As our national debt continues to rise in volume, financial markets will become concerned that risk is rising in terms of the U.S. government being able to pay back those loans, even if marginally, and perhaps pressure interest rates to rise or stay at relatively high levels. Equity markets like lower interest rates on American debt securities because the opportunity cost of continuing to buy and hold equity positions falls and draws investors toward stocks. But when interest rates rise, it means investors may liquidate their equity positions, take the cash, and move it into national debt securities (Treasury securities or “Treasuries”) that have rising interest rates. We have avoided most of those effects to date because the debt management has been to refinance old debt by issuing new debt when interest rates fall. Such actions manage the total cost of debt as the volume of debt rises.

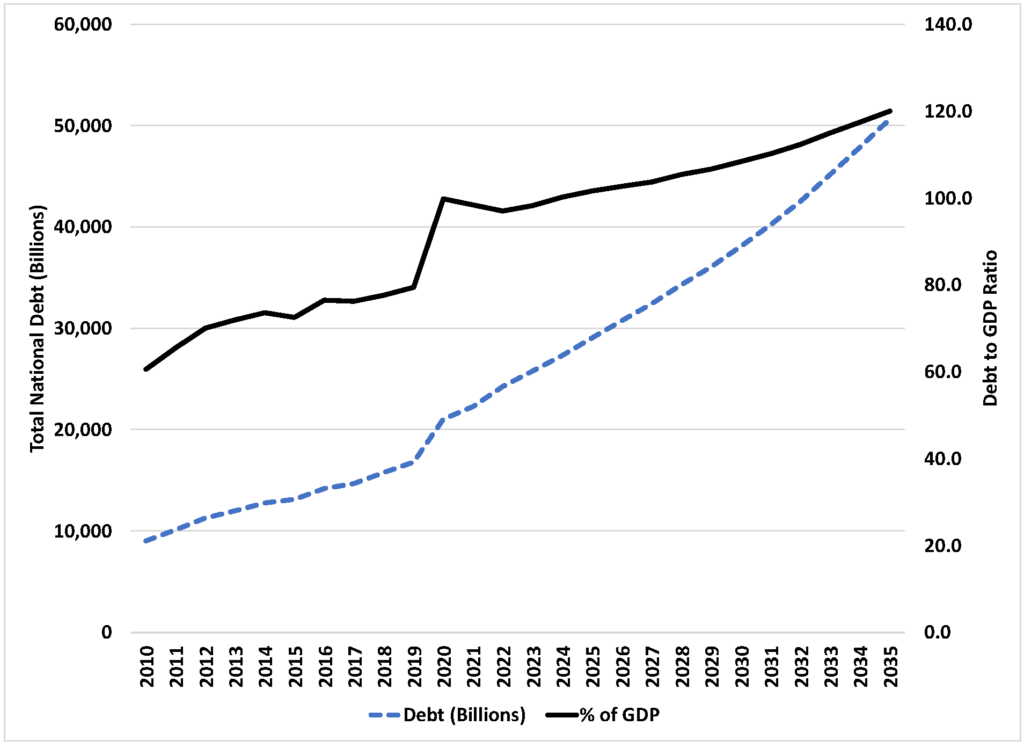

The following graph shows the latest forecast of debt levels for the United States government (these data do not include outstanding corporate or household debt, this is just the federal government’s borrowings). I am also including the debt-to-GDP ratio and the forecast (think the amount of borrowing to the amount of income generated by the United States economy in one year as a hand-wavy measure of government solvency). These data come from the Congressional Budget Office (CBO).

The higher the debt goes, just like at home, the rising volume puts pressure on the federal government to generate income to either service the debt (pay interest payments) or to repay the debt and reduce the overall debt load. Rising debt levels also increase the risk of rising taxes, especially in certain government programs. Government programs closely associated with federal debt levels are Social Security and Medicare. These programs take collected tax dollars and invest in Treasuries as a way to save for future claims. The stability of those programs, due in large part to demographic changes, is another potential need for the government to borrow. Because of rising claims and use of funds, both these programs have pessimistic outlooks without more borrowing, higher tax rates, or both.

Do the changes in the figure above suggest relatively high interest rates are here to stay? Rising interest rates on our federal government’s debt do pressure other interest rates and make the cost of borrowing money rise for all businesses and households. Investors will surmise the true nature of risk in the federal debt market over the next decade. As those investors ask for more risk coverage, we all face higher costs of borrowing and doing business.