North Bay businesses from manufacturers to wineries are “self-insuring” against wildfire risk to remain eligible for commercial property insurance. The term refers to a wide range of activities, including home hardening, forest fuel reduction and grazing uncultivated land. Despite the proactive undertakings, insurers who still offer policies in the North Bay have increased premiums in the last four years, typically by between 400 and 1,000%.

“The revenues in the wine industry are nowhere near big enough to cover the massive cost of insurance,” says Cyril Chappellet, chairman of the board of Chappellet Winery in St. Helena. “That’s why we developed so many interlocking strategies to put out fires and prevent the spread of fire between structures.”

Insurers that decide they need a rate hike, but have not yet requested one from the California Department of Insurance, may ask for one soon. Customers can expect further increases in the next few years, says Janet Ruiz, spokesperson for the Pennsylvania-based Insurance Information Institute, the national trade association for the insurance industry.

“Inflation has slowed. This does not offset increases in costs to rebuild and compensate a business for loss of income when it is closed. Those two expenses have increased in the past four years because of rises in costs for labor and supplies,” says Ruiz.

As businesses reduce their wildfire risk, insurers may reduce their rates. This is not occurring right now.

Businesses and insurers are waiting to see how the market is transformed by the California Department of Insurance’s (CDI’s) implementation of its new Sustainable Insurance Strategy. The changes are set to impact the market by mid-2025.

One of the biggest shifts is the CDI will allow insurers to use technology that predicts catastrophe modeling. In the past, insurers could only use historical data. The CDI will also take measures to encourage property owners to leave the California FAIR Plan, aka Fair Access to Insurance Requirements, a state insurance-industry program to provide insurance to high-risk homeowners and businesses that can’t find fire coverage. The latter move is meant to draw residential and business customers back to the insurance marketplace.

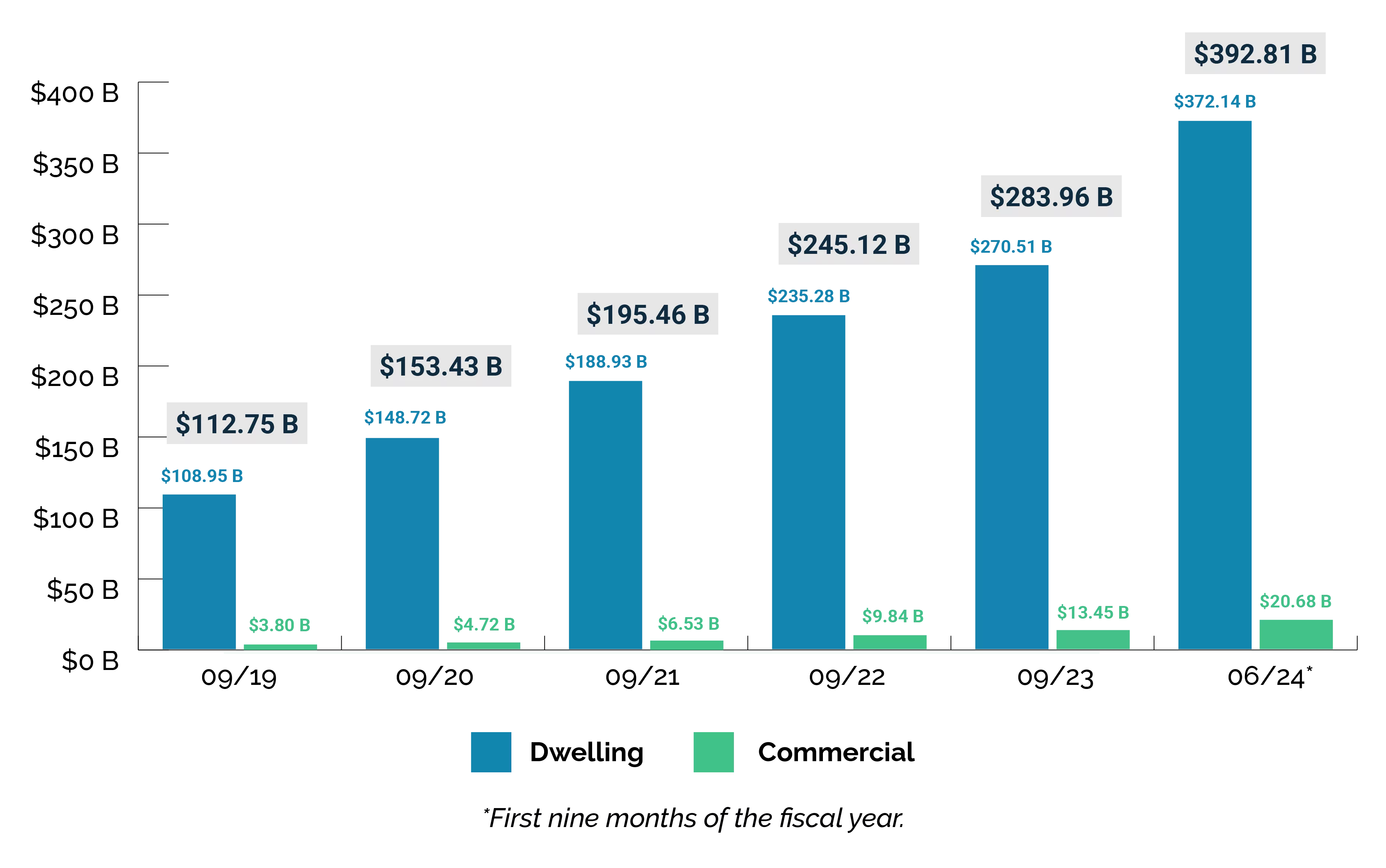

The CDI is concerned that the number of high-risk policies that the FAIR Plan has written threaten its solvency. In June 2024, the FAIR Plan’s total exposure was $393 billion, a 38.3% increase since September 2023.

It is now common for North Bay customers to layer together multiple policies to insure a business. A winery may have a policy with one insurer for their property, a second for their equipment, a third for their vehicles and a fourth for their wine, if they can afford the last expense.

In past decades, insurers offered discounts and other incentives to buy multiple types of insurance from a single carrier. Now a customer will work with a broker and multiple carriers to “break the bundle.”

The California legislature could help by amending state insurance code to distinguish the terms “wildfire” and “fire,” says David Capponi, partner in Malloy, Imrie & Vasconi Insurance Services in Napa.

“If insurers can treat wildfires differently from other types of fires, local businesses can choose to buy that insurance or not,” says Capponi. “I see a wildfire as inherently different from a house fire. A wildfire spreads because of high fuel loads in forests and dryness due to climate change. It is a catastrophic event that affects a wide geographic range, like an earthquake.”

As a co-owner of Piña Napa Valley Winery in Napa, Capponi would decline wildfire insurance solely to have the ability to buy coverage on his wine stock.

“Because of the ‘fire’ definition including all fire, it is an all-or-nothing deal for property insurers. If they can’t accept the ‘wildfire’ risk, then they can’t provide any property coverage,” says Capponi.

He adds California is a good state to write policies if the risk of wildfires is removed from policies.

“We now typically have seasonal heavy rains. We do not have widespread threats of tornadoes, hurricanes, hail storms and ice storms. The North Bay especially has many properties that are high value, which equates to premiums that make money for insurers. The question is how to encourage policies to be written differently,” says Capponi.

Ideas for fire defense

North Bay businesses can protect themselves from wildfires by expanding upon the strategies that Cal Fire has developed for residential structures. Cal Fire recommends establishing at least 100 feet of defensible space around every building, reducing potential fuel within 100 feet or to the property line and clearing areas within 10 feet of propane tanks down to bare mineral soil.

The agency advises placing dumpsters a fair distance from structures. An owner should also place them inside a fire-resistant enclosure and keep the lids secured from blowing open.

“This decreases the chance of embers igniting in trash and being carried to buildings, and vice versa. A business owner should also keep flammable objects like paper documents and bags of fertilizer out of openings like doors and windows. As a general rule, they should close doors and windows, especially on windy days,” says Frank Bigelow, deputy director of Community Wildfire Preparedness & Mitigation and Fire Engineering & Investigations Division of Cal Fire.

“If you are not cultivating burned or tilled land, nature will seed the ground for you. You want to avoid the spread of noxious species like star thistle, an annual weed that can grow extremely tall,” says Cori Carlson, president of Napa Pasture Protein in Napa.

Grazing animals can assist with many of Cal Fire’s suggestions regarding vegetation, including managing annual grass growth, reducing brush and creating vertical space between trees and ladder fuels like grass.

“Our services make it possible for businesses to preserve oak forests and tree cover in general by eliminating fuels that create high-intensity fires,” says Carlson.

A combination of grazing animals and hand crews is also effective, says Johnnie White Jr., partner in Piña Vineyard Management in Rutherford.

“We offer both types of services, often in combination. People can see the risks that animals cannot. They can also perform additional tasks like wood chipping. We often partner with teams from other entities, like neighborhood Fire Safe Councils. We’ve built fire breaks on ridges and built fire roads along the backs of properties to give fire crews access to isolated areas,” says White.

Chappellet Winery, located on Pritchard Hill east of the Silverado Trail, sees reducing fire risk as an ongoing effort.

“We’ve got two fire engines, a water truck, a trained team of eight employees, a trailer with fire hoses, fittings and nozzles and fire-retardant gel that coats brush and structure walls. That’s just the beginning,” says Chappellet.

The business is in oak woodlands. This means the team regularly removes brush and downed limbs in the forests. They do this up to a height of between 6 to 12 feet.

“That way embers which fall from the canopy have little to burn when they hit the ground. We also expanded our defensible space around buildings to between 100 and 300 feet. In addition, we put sprinkler systems on top of the buildings, to wet the top and put out embers,” says Chappellet.

The winery made so many upfront investments between 2018 and 2022 that it is now in a “maintenance phase.” This lower level of spending runs several hundred thousand dollars a year.

“Anytime we think of something new, we evaluate it and consider adding it,” says Chappellet.

Discoveries from fire researchers

Fire researchers across the country are finding a property owner cannot pick and choose specific types of protections.

“You need to do it all. Look at your property in a holistic way. Also consider the risks to and from your neighbors’ properties,” says Alexander Maranghides, fire protection engineer at the National Institute of Standards and Technology (NIST) in Maryland. NIST conducts research in partnership with Cal Fire as well as other state and local entities across the U.S.

NIST’s experiments show fire spreads like a domino. It establishes paths through a property by generating flames and embers.

“You do not want flames hitting your structures. You also have to protect against embers,” says Maranghides.

Taking such measures includes reducing materials for flames to consume and making sure openings like windows are secured and do not line up. It is also necessary to harden structures.

“If you want to protect the interior of your structure from embers, use California state-rated vents to prevent embers from entering areas like the crawl space and attic,” says Maranghides.

Accessible Dwelling Units and combustible sheds present concerns.

“They will produce both flame and ember exposures. They can ignite vulnerable structures nearby and contribute to fire spread across the community by generating embers. Place them far away from other structures, from barns to homes,” says Maranghides.

Establishing fuel breaks on a property is helpful in disrupting fire pathways. Fuel breaks can include portions of forest with brush and lower limbs of trees removed. Fuel breaks can also consist of roads, maintained rows of wine grape vines, waterways like creeks and grazed lands.

Hawks served with Cal Fire from 1989 to 2022. He now helps conduct experiments for IBHS in Chester County, South Carolina.

“Our work shows simple things make a difference, like storing pallets and boxes far away from structures. For windows, use dual pane tempered glass. Tempered glass provides a much higher level of heat resistance to protect against direct flames and radiant heat,” says Hawks.

A business should be able to close and secure any ventilation systems on a roof. Also, an owner should not place combustibles around structures, particularly within the first five feet. This increases the risk of the buildings or walls catching on fire and exposing other structures to flames, radiant heat and embers.

One of the issues Hawks saw in Napa County was large openings in structures that are vulnerable to embers.

“Having a garage-style metal door that you can close very quickly reduces the risk of embers freely flying inside,” says Hawks.

Business owners can hire a consultant to help with these tasks. Third parties can help educate staff and suggest improvements.

Adam Iveson, co-founder of Ember Defense in Reno, has serviced several thousand clients in Marin, Napa and Sonoma counties since 2019.

“We start by conducting an onsite evaluation and share tips for structure hardening and defensible space. We look at their vents, gutter guards and other entry points for embers intrusion, then provide options on how to mitigate those risks. We only recommend products like Vulcan Vents and FireStorm Gutter Guards we’ve vetted through our work,” says Iveson.

Ember Defense has developed an “Ember-Certified” contractor network of professionals who can assist with product installation. In addition, the company offers “Guardian Wildfire Packages,” a concierge wildfire program that assists property owners with all their wildfire needs, including understanding the insurance process.

“In June 2024, we deployed our crews on-site for four days, switching out shifts and working with local agencies. This effort protected a Guardian Client’s property in Healdsburg from being destroyed by the Point Fire,” says Iveson.

Ember Defense uses drones and different software programs to assess fire risk.

“Such tools cannot replace ‘boots on the ground,’ people who physically assess a property as a whole,” says Iveson.

Iveson says the North Bay leads the state in understanding and working with vegetation.

“This part of the state is light years ahead of other regions. Fire Safe Marin has been a leader in advocating wildfire safety and fuel management since the Oakland-Berkeley Hills fire in 1991. Yet, the North Bay needs to increase the amount of structure hardening. There are tens of thousands of structures that need better protection,” says Iveson.

The California Farm Bureau is watching how the North Bay handles fires to apply lessons learned to other agricultural areas, says Peter Ansel, senior policy advocate for the California Farm Bureau.

“What affects the agriculture business in the North Bay is the same as what’s happening statewide. The North Bay has so much wine grape cultivation that a lot of owners have made substantial investments in fire protection. We want to see what works, so our members can concentrate on farming,” says Ansel.

He adds when agriculture business owners have to spend a considerable amount of time finding insurance and developing strategies to purchase it, this shifts their concentration away from farming.

One of the changes that will help businesses and insurers going forward is the creation of rules that clarify what homeowners in high wildfire risk areas can have in a 5-foot area near their structures. This area is also called “zone zero.”

The rules are currently being developed by the California Board of Forestry, which is part of the California Natural Resources Agency.

“We are still in the pre-rulemaking phase of development on zone zero,” says Tony Andersen, deputy secretary for communications for the California Natural Resources Agency. “Board staff aims to have a draft proposal to present to the Board of Forestry as soon as is feasible, most likely in early 2025. Until then, we continue to evaluate options for phased implementation over time. We are weighing factors such as cost to property owners and the relationship between these regulations and those recently promulgated by the Department of Insurance,”

Insurance brokers learn to showcase

Insurance brokers and agents who serve the North Bay are looking to explain the benefits of changes that property owners are making to insurers. They describe such actions as “leaning into mitigation.”

“Having a detailed explanation of your wildfire mitigation efforts to share with your broker is extremely helpful. While some properties have gone to great lengths to minimize risk, the insurance market remains challenging. (It) is not providing the level of discounts property owners need to reduce their costs” says Debra Costa, senior vice president and vintner practice leader at Heffernan Insurance Brokers. The company is headquartered in Walnut Creek and has offices in Napa and Petaluma.

Insurers often limit the amount of risk they carry for certain zip codes, like 94574, which covers areas directly east and west of Highway 29 near St. Helena. Once insurers hit this limit, they often stop writing new policies.

“This is why we work with clients well in advance of their renewal dates. We also advise clients to develop a recovery plan for certain elements of their business to avoid substantial loss of income,” says Martha Bane, managing director of property practice and a principal in the Real Estate and Hospitality practice for Gallagher. Gallagher is a global insurance brokerage firm headquartered in Illinois that has clients in the North Bay.

The supply chain for construction materials and equipment has now recovered from disruptions. Still, having a plan in place is a good tip for business owners. Demand for rebuilding and measures to continue business operations can surge after a severe wildfire.

Another option for business owners is to buy coverage from a non-admitted insurer. This type of insurer does not follow the same state regulations as an admitted insurer. The advantages of working with a non-admitted insurer are that it can currently use predictive wildfire modeling and alter policy prices without state review.

Non-admitted insurers can be more willing to take on customers in the North Bay. They may offer policies at lower prices than admitted insurers.

“Delos Insurance Solutions, which is based in San Francisco, currently offers home insurance policies for property owners in areas where wildfires are common. We are looking to move into commercial property insurance,” says Andrew Notohamiprodjo, head of data at Delos Insurance Solutions.

Delos recommends its customers ask local governments and Fire Safe Councils to utilize broader measures to decrease risk, like controlled burns.

“Our research has found that it might take community level changes to mitigate wildfire exposure. Those changes could give us the ability to write more policies and decrease premiums for a given area,” says Notohamiprodjo.

There is hope in the next five years that fire prevention efforts by Cal Fire, cities, counties, large private property owners and Fire Safe Councils will regularly show up in admitted and non-admitted insurers’ models.

“That’s why using predictive modeling is helpful. It’s also why individual and group progress on everything from wood chipping to forest fuel reduction makes a difference in pricing,” says Notohamiprodjo.

Five tips for reducing wildfire risk

- Tour properties that experienced destructive fires and see how they rebuilt. For example, Signorello Winery, which is on the Silverado Trail in Napa, put its power lines underground, bought backup generators and has fire pumps on its water supply.

- Tour or look at aerial photos of areas affected by recent fires like the 2024 Point Fire in Healdsburg. Talk to firefighters, insurers, fire risk consultants and property owners to learn what it took to stop these fires.

- Work with a contract grazing business to create fire-fuel breaks to protect the land, infrastructure, residences and businesses on or surrounding a property.

- Consider replacing non-native species with lower growing native grasses with lower fuel heights. Work with the local Resource Conservation District for further advice.

- Talk with vineyard management company owners about what services hand crews can offer to reduce fire risk. Ask about their regular seasonal schedules.